As the end of the year approaches, we close the books on another production year. There are many lessons to be had this year, but none of them greater than “Cash Flow is King.”

If you did not learn this in the ’80s, it is a guarantee that your parents or grandparents did.

Making mistakes is an inevitable part of the human experience. What you learn from your mistakes is what really matters. Making the same mistake twice is not a mistake but rather a choice.

For years, we have been preaching the importance of raising farm transition decisions to a conscious level. Now more than ever, it is important to know what cash flow situation your farming heir will be facing at the time of transition.

A corn yield of 200 bushels per acre in 2022 with $6.20 cash corn would produce $1,240/acre of gross revenue. The Iowa State University Ag Decision Maker tells us that the average cost of corn production is between $968 and $1,066 per acre (using $285/acre for land acquisition costs). There was still a chance for profit with $6.20 corn.

The same yield of 200 bushels per acre in 2023 with $4.70 cash corn is $940/acre of gross revenue. With input and land acquisition cost between $968 and $1,066/acre, there is a loss (not a profit).

There are many variables in profitability, but owning your own land without debt can make or break families in the coming years. Two-thirds of our farmland is owned by individuals 65 years and older. Age 75 and older owns one-third of farmland. A majority of these acres have no debt.

There is a very small portion (less than 15%) of land owned by those under age 55. A majority of that land ownership has debt. Anyone in that age group will have a hard time competing with the required subsidization to acquire land, particularly with escalating interest rate. Does this situation sound familiar?

Who will own the land after those who are age 75 pass (on average) in the next 10 years? This is concerning for our industry.

Purchase payments

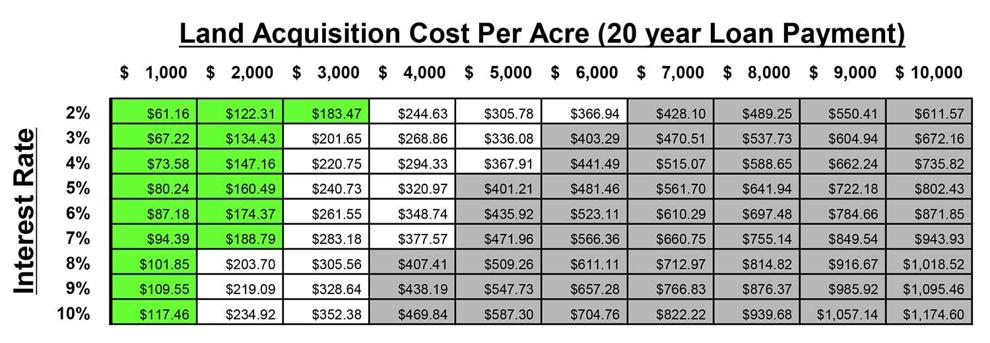

Here is a table that you can use to quantify the cash flow required for a 20-year loan given an interest rate (ranging from 2% to 10% on the left side of the table) and an amount borrowed per acre (ranging from $1,000 to $10,000 on the top of the table).

The green section of the table shows annual payments per acre for the combination of interest rate and land acquisition (loan principal) amounts that would require a payment of less than $200 per acre.

The white section would require an annual payment per acre between $200 and $400 per acre. This is the range where most farmers are comfortable with land acquisition payments.

The gray section would require a cash flow for land payments of $400 per acre or more.

Many may scoff, as this table does not even go beyond $10,000 per acre and land may be selling in their area between $15,000 and $20,000 per acre. There was no need to waste the space printing loan options over $10,000/acre with no chance of that loan cash flowing.

People are also reading…

Cash flow exercise

In an effort to raise the awareness of farm transition cash flow issues in the estate settlement process, we run the audience through a farm continuation exercise at the end of each workshop.

Each participant receives a worksheet designed to calculate their own individual farm continuation number for land acquisition within “their own family” with “their own numbers.”

The worksheet estimates the number of acres, estimated price per acre, current land debt, number of children and sweat equity.

It is fascinating to experience the emotion in the audience participation. Most folks understand the issues exist, but have not had the opportunity to quantify their own predicament.

In one recent workshop, a landowner thought that his second spouse and six children (and their combined five spouses) would “more than likely” agree to keep the land in the family (without any mention in his will of a plan). The group quickly shot this notion down.

Another felt it was necessary to have a 50% discount on land values at death, while another objected to this proposal of “fairness” and felt that any discount would not be fair to the non-farming heirs.

One young farmer estimated his annual payment for buying 200 acres of family land would be $128,000 ($640/acre). He recognized that he would have to pay income tax on principal payments (only interest is deductible).

With a majority of Iowa farmland owned by those age 65 years or older, the substantial distribution of farm estates in the next 10-20 years could produce insecurity in our communities.

The reality is that it is impossible for a farm heir to buy the family land in the one-year period of an estate settlement that may have taken a lifetime for the family to accumulate in the first place.

My hope is that each of you has a conscious awareness of your “farm transition number” in the current economic environment. Only you (and maybe your banker) can decide how much you are willing to subsidize for future land acquisition.

For 31 years, Steve Bohr has been a partner in the farm continuation firm of Farm Financial Strategies, Inc. For additional information on farm continuation issues or if you have a question please contact Steve via email at Bohr@FarmEstate.com or by phone at 800-375-4180.